In previous installments of this multi-part private equity (PE) series, we learned about PE, its interest in ophthalmology practices and ambulatory surgery centers (ASCs), and the pros and cons of selling to PE from various experts. In this article, we discuss the PE sales process from preparation to completion for the seller.

As the number of private equity (PE) transactions continues to increase, we can benefit from the wisdom gained by pioneering practices and surgery centers that sold to a PE firm early on.

One of my favorite questions to ask my clients or peers is, “If you had to do it over, what would you do differently?”

Based on their answers, and the collective experience of my BSM Consulting colleagues, this article details a typical transaction process, with special emphasis on who should be in-the-know and when.

Defining the Transaction Process

I often use the analogy of relationship milestones to track the PE transaction process; after all, you are heading into a long-term commitment. However, just as an individual should understand his/her own needs before entering a relationship, practices need to identify what they hope to gain through PE transaction before searching for a partner.

Prep Work: Identify Needs

Ideally, your business strategy and needs will be clearly defined before you express interest in a potential suitor. Host a strategy session with owners to discuss long-term goals for the practice and ASC. As part of this discussion, I recommend involving key business advisors — preferably with transaction experience — to help avoid pitfalls and wasting time. In my experience, such individuals can shed light on whether a practice should pursue PE or remain independent early in the process.

Once you have assembled your team, some questions to ask include:

- What is the vision for growth?

- What external forces does the business face?

- What organizational values do you want to remain intact?

- How will an investor help you meet your goals?

- What will you give up by selling?

Communication at this stage of the transaction process should be confined to a small, trusted circle. Make it clear to all parties that there is no benefit in disclosing anything this early on. There is a likelihood that a transaction may not occur; and, even if it does, it is at least a year away. Therefore, mentioning that a sale is being considered will only disrupt day-to-day business operations and cause staff to worry needlessly.

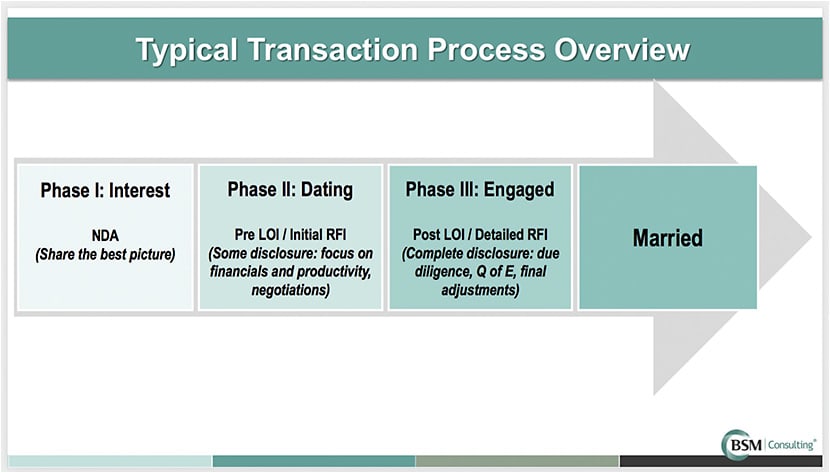

Phase 1: Mutual Interest

Assuming the strategy session directs you to pursue a potential sale, it’s important that you take the time to get your practice in order before stepping out onto the dating scene. Conducting a financial and an operational review of your business are the natural next steps. Below is a breakdown of what activity should take place during this phase of the process.

- Understand your financial opportunity. Although quality patient care is the most important aspect of ophthalmology businesses, this phase is dominated by reviewing the financial opportunity. You need to conduct your own financial assessment to determine reasonable value.

- Identify potential partners. Given your strategy and values, ask yourself: to whom would I be willing to commit for a long-term relationship?

- Dress up. In other words, identify the most attractive aspects of your business and be prepared to promote it to a potential partner. This may happen simultaneously with the first two steps.

- Go out on the town. Equip your confidential advisors with a promotional piece (omitting the actual name of the practice and ASC), so they can share the attractive aspects of your business and make clear your intention of finding a financial partner. Hopefully, this will generate interest from various suitors.

- Express a willingness to date. Before divulging too much information, determine whether your suitor’s interest is strong enough. If it is, sign a non-disclosure agreement before sharing information.

During this phase, it is still wise to keep communication limited to owners and a select few business advisors. Directing staff members to carry out the above assessments might lead them to suspect what’s happening. To keep staff involvement (and suspicions) contained, consider using a business advisor, a legal advisor, an accounting advisor, and possibly a broker or investment banker (preferably with transaction experience) to handle the above steps.

Phase 2: Dating

During the dating phase, both parties generally put their best foot forward. This means you and your advisors will be presenting your “profile,” or the story of your business, in the hopes of becoming serious with your partner and attracting a proposal offer. More specifically, in this stage of the relationship you will:

- Divulge more about your practice. Potential suitors will send a request for information to get to know your business better.

- Share snapshots. In the first phase you dressed up. Now, you are showing snapshots of your business. This includes, but is not limited to, key people, locations, growth, company history, differentiating factors, and, of course, detailed financial information.

- Have heart-to-heart conversations. During the dating phase, initial negotiations begin. Serious conversations about the price and terms of a deal will occur.

While the relationship is beginning to get serious, at this point it is still blossoming. As such, it is not yet ready to be shared with everyone. Only your closest companions — namely, executive staff and owners — should have knowledge of this potential partnership.

Phase 3: Engagement

A proposal in the business world is the Letter of Intent (LOI). This offer from the buyer details the transaction, including key terms, the forthcoming process, and, of course, the price. Once signed, you enter an exclusive period (or engagement) with the buyer. It is at this point in the relationship that full due diligence is conducted. Expect the following steps:

- Share everything. During due diligence, you share all details — every … last ... one. For this reason, it may be necessary to involve more staff, as appropriate.

- Verify your finances. At this point, you must provide all supporting evidence that the revenues and expenses are accurately represented. This includes detailed, complete transaction files from your practice management and accounting systems. Because there are MANY questions to be answered, you will need to loop in individuals involved in creating and implementing the financial policies that resulted in handling transactions. Depending on the findings, it is not uncommon for the offer to be renegotiated at the end of this step.

- Create your prenup. If the new offer and terms are still acceptable, it is time to draw up the legal documents.

During the third step, most of the providers will need to be involved as new agreements will need to be signed to close the transaction. As the circle widens, the likelihood that anything will be kept secret diminishes. Developing a carefully laid-out communication plan with a thoughtful, encouraging message will minimize anxiety and ensure a smooth transition. Begin by looping in trusted practice and ASC leaders as the due diligence process unfolds. Depending on the level of engagement you have with your advisors, it is likely that your trusted leaders will need to be involved in gathering information throughout this phase. As the process unfolds, divulge the pending union to providers, then the management team, and finally, staff. By following this order, you are demonstrating respect for the practice’s internal hierarchy.

Marriage

Once the team knows and the documents have been signed, you are officially in a committed relationship. Now that the courtship process is complete, you can begin the real work of building the relationship and moving toward your shared vision — hopefully, the beginning of a beautiful, mutually beneficial partnership. ■